Everything You Always Wanted to Know About Indirect Costs (But Were Afraid to Ask)

This is a guest post from Jeremy M. Berg, who is currently Professor of Computational and Systems Biology at the University of Pittsburgh. Berg received his B.S., M.S., and Ph.D. degrees in chemistry. He started as an Assistant Professor of Chemistry at Johns Hopkins University in 1986. He moved to the Johns Hopkins School of Medicine as Director of the Department of Biophysics and Biophysical Chemistry in 1990. In 2003, he became Director of the National Institute of General Medical Sciences (NIGMS) at NIH. He served at NIGMS until July 2011 when he moved with his wife Wendie Berg, M.D., Ph.D., a leading breast imaging researcher, to the University of Pittsburgh. Berg served as Editor-in-Chief of the Science family of journals from 2016-2019.

Few topics relevant to research produce more confusion and, in many cases, acrimony, than so-called “indirect costs”. This term, also referred to as “Facilities and Administrative Costs”, relate to research costs that are not readily attributable to any specific project. This turmoil is due to two primary issues and their consequences.

First, the estimation of indirect costs is inherently complicated and arcane. This requires considerable accounting and access to lots of institution-wide data. Second, both institutions and the government have not worked to make indirect costs even reasonably transparent. Indeed, in some cases, some organizations have gone out of their way to obscure important information.

These two factors have inevitable consequences. Many people, including most faculty who bring in federal grants as well as some governmental officials at funding agencies, do not understand indirect costs. In some situations, investigators may perceive that indirect costs represent an unfair tax on the grants that they bring into their institutions. In the political context, indirect costs are an easy target for those with other agendas regarding science funding and universities. Throughout this discussion, it is important to know that the recipients of federal grants are the institutions from which the applications arise, not the investigators.

What are indirect costs and how are they determined?

Many different costs are associated with conducting research. “Direct” costs include full or partial salary for the principal investigator and for others involved in conducting the research, costs for reagents and other supplies, and other expenses depending on the project. This first group of costs are relatively easy to assign to a specific project and the associated grants.

There are other costs of conducting research that are “indirect” and are difficult to attribute to a specific research study. These include costs of heating, cooling, and cleaning laboratory space, administrative costs related to personnel and other aspects of the research (e.g. institutional review boards, grants management/accounting, conflict of interest management), depreciation of laboratory and office space (which reflects the fact that these lose value over time due to wear and tear), animal care and use facilities, and so on. Only some small fraction of each category is related to any given project.

At some points in time and, still, in some systems in other countries, the second group is treated as direct costs with a requirement for estimating the amount in each category to assign to each project. Around the beginning of the 1960s, a more efficient process was developed. This was based on the insight that indirect costs only need to be reconciled at the institutional level, not at the level of individual grants. For each institution, an overall indirect cost rate was determined essentially by looking at all the indirect costs across the institution and dividing by the sum of the direct costs. One important adjustment is that some direct costs are excluded from indirect cost calculations. Examples include small equipment since this is generally housed in space already used for research and the equipment does not require any administrative expenses. Aside from the cost of the experimental intervention itself, many patient care costs associated with clinical trials (such as blood work or costs of treatment related to side effects from the experimental intervention) can be reasonably assumed to be covered by the hospital or health care system/insurance as part of patient care. Removing such costs results in what are called “modified total direct costs” (MTDC) which is then multiplied by the indirect cost rate to yield the indirect reimbursement due.

The principles for negotiating indirect costs for educational institutions are described in 2 CFR 220, formerly known as OMB Circular A-21. The principles for other non-profit institutions including independent hospitals and free-standing research institutes are governed by a slightly different document 2 CFR 230. Indirect costs are broken down into “facilities” and “administrative” costs. Importantly, the administrative portion of indirect costs has been capped at 26% since 1992 for educational institutions under 2 CFR 220 but is not capped for hospitals and research institutes.

Indirect cost rates are calculated across the federal government rather than agency by agency. In other words, at a given institution, the indirect cost rate is the same for a grant from the National Institutes of Health as it is for the National Science Foundation. Each institution negotiates its indirect cost rate with one of two centers within the government. For institutions that tend to do more biomedical research, rates are negotiated with an office within the Department of Health and Human Services (not the NIH) and are typically negotiated every four years. For those that tend to do more physical sciences research, rates are negotiated within the Office of Naval Research and are typically negotiated annually.

Again, once a negotiated rate is agreed to, the amount of indirect costs for each grant is calculated by taking the direct costs for the grant, removing some of the costs not subject to indirect costs to yield the MTDC, and then multiplying by the indirect cost rate.

To give a concrete example, suppose that a project has direct costs of $300,000, with $90,000 of that attributable to equipment not subject to indirect costs. Assume that the indirect cost rate is 55.0%. The indirect costs due would be 0.55(300,000 – 90,000) = 0.55(210,000) = $115,500. The total costs received would be $300,000 + $115,500 = $415,500, and the percentage of the total costs due to indirect costs would be $115,500 / $415,500 = 27.8%. These values are typical for actual indirect costs as will be discussed subsequently.

Key aspects of Indirect costs are explained well and engagingly in this short video:

.

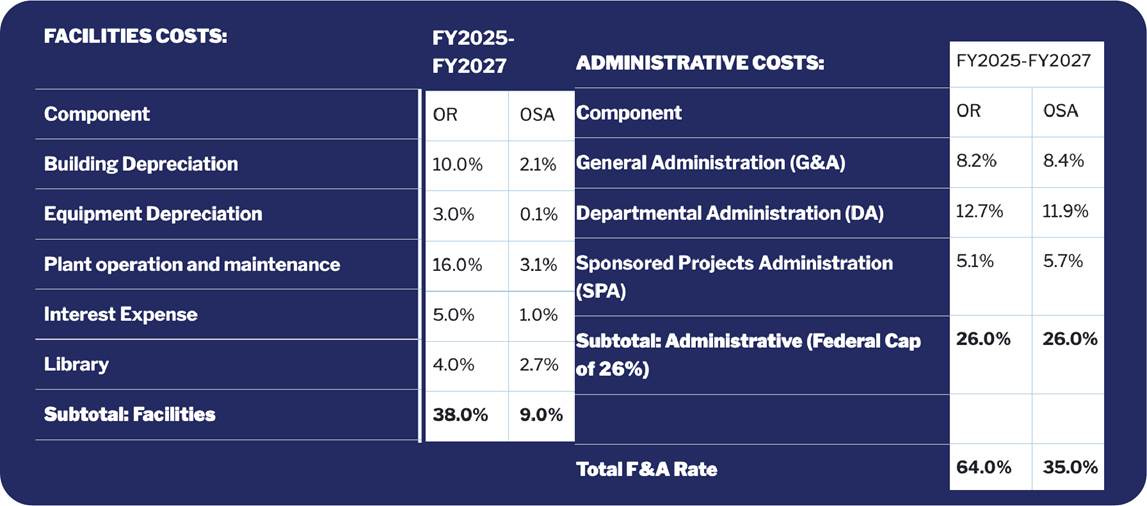

Details about indirect costs are, unfortunately, difficult to find. Universities rarely share the components that contribute to indirect costs and that results in a continued sense that they are hiding something. However, occasionally, some universities do share some details. For example, Princeton has this information on their website, which I recently stumbled across.

Here “OR” refers to Organized Research (that is, research that is conducted in campus facilities) and “OSA” to Other Sponsored Activities (often performed off-site). This reveals the dominant categories that constitute the indirect cost rate. Unfortunately, since similar data are not readily available for other institutions, it is not possible to examine how these components vary from institution to institution. Note the capping of Administrative Costs at 26.0%.

Common misunderstandings about indirect costs

Indirect cost rates are determined by the funding agencies

Many believe that the funding agencies themselves play a role in setting indirect cost rates. As noted above, two centers (termed “cognizant agencies”, one in the Department of Health and Human Services and one in the Office of Naval Research) negotiate indirect cost rates. Each organization deals with only one of the cognizant agencies.

There should be different indirect cost rates for different grants with the first grant to an investigator receiving a higher rate, but subsequent grants receiving low rates

In terms of actual indirect costs, this may seem to make sense. It seems that the first grant to an investigator has indirect costs that should cover most lab space and administrative costs. Thus, indirect costs for the second and subsequent grants should be lower. However, this does not reflect how the indirect cost rate is determined based on research activities pooled across the institution. Alternative models with higher indirect rates for the first grant and lower rates for subsequent grants are certainly conceivable but the total amount of indirect costs going to the institution would not change. Since indirect costs are negotiated based on actual data about costs and well as projections about how much funded research will occur, this applies to all institutions regardless of scale.

Indirect costs are returned to investigators at some institutions

It is a practice at some institutions that the dean’s office “returns indirect costs to investigators” under some circumstances. This is purely an accounting device intended to incentivize seeking and winning more grant funding. Indirect costs cover (but usually not in toto) real costs related to research. Funds must be expended for research to proceed: Administrators who manage compliance issues must be paid. The notion of “returning indirect costs to the investigator” is purely accounting. Unfortunately, this has contributed to the notion that indirect costs form slush funds that can be used for any purpose. Note that some costs of departmental administration are allowable indirect costs as the Princeton example about illustrates.

Institutions make a profit on indirect costs

This appears to be a widely held view, but it is inaccurate. Indirect cost rates are negotiated based on actual expenditures. The full costs associated with research are not, in fact, covered. This is due in part due to the cap on administrative costs (put in place in 1992) while administrative expenses related to compliance have increased substantially. Indirect cost rates are negotiated based on projections of future research activities so institutions can do a bit better, in terms of better indirect cost recovery, if they beat those projections but, even in the best case, they still are unlikely to cover their full indirect costs.

The February 7th, 2025 NIH indirect cost rate notice

On February 7th, 2025, a notice was posted by NIH (although it was not written nor vetted by anyone at NIH) that asserted that indirect cost rates would be capped at 15%. This notice caused great concern across the academic community. The approach described in this notice has been challenged and found to be illegal, including in a recent appellate court ruling I will discuss subsequently. This notice also is based on some misstatements, perhaps made from ignorance. Here is one key passage:

Although cognizant that grant recipients, particularly “new or inexperienced organizations,” use grant funds to cover indirect costs like overhead, see 89 FR 30046–30093, NIH is obligated to carefully steward grant awards to ensure taxpayer dollars are used in ways that benefit the American people and improve their quality of life. Indirect costs are, by their very nature, “not readily assignable to the cost objectives specifically benefitted” and are therefore difficult for NIH to oversee. See Grants Policy Statement at I-20. Yet the average indirect cost rate reported by NIH has averaged between 27% and 28% over time. And many organizations are much higher—charging indirect rates of over 50% and in some cases over 60%.

This statement said that “the average indirect cost rate reported by NIH has averaged between 27% and 28% over time”. It is true that indirect cost recovery (indirect costs paid, divided by total costs paid) have averaged 27-28%. But these are not indirect cost rates. This difference is due to (1) the fact that some direct costs are excluded from indirect cost calculations (as noted in the discussion of MTDCs above) and (2) Indirect costs are determined by multiplying the indirect cost rate by the MTDC whereas the 27-28% figure is the percentage of total costs. Thus, if the indirect cost rate is 50% and all direct costs were included, the percent expenditure would be 0.50 (DC) / (DC + 0.50 (DC)) = 33.3%. Thus, this statement is an apples vs. hummingbirds comparison which serves to create the false impression that many organizations are extracting substantially more indirect cost reimbursement than they are due.

Legal Issues

As noted above, the 15% cap was not implemented because organizations, including the American Association of Medical Colleges, quickly sued claiming that the proposed policy was illegal. The lawsuits were successful and have been upheld on appeal. The primary reason is that Congress established the indirect cost rate negotiation process and routinely incorporates language about this process in appropriation laws. Thus, any changes to the policy would have to developed by Congress and passed into law.

Negotiated Indirect Cost Rates and Indirect Cost Recovery

Negotiated indirect costs rates are necessary for applicants to complete grant applications, and they can generally be found on organization websites through (sometimes persistent) internet searches. Unfortunately, they are not compiled in any central location, and, in some cases, the information is password protected or only available from inside institutional networks.

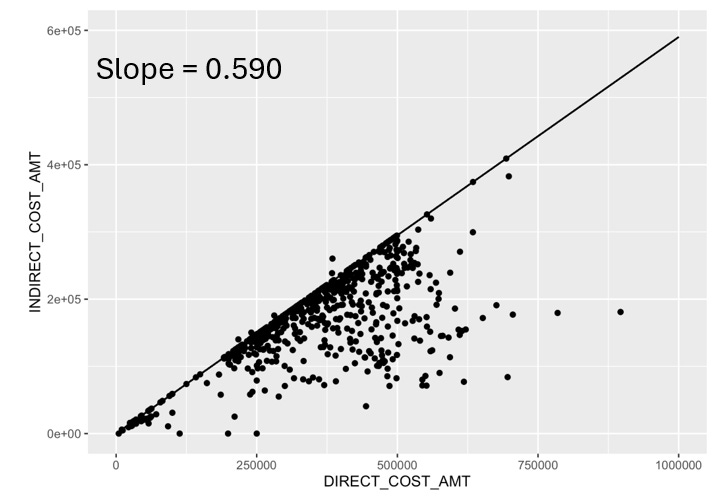

However, I discovered that they can be readily deduced from data publicly available from NIH Reporter. For institutions with a reasonable number of grants (50 or more) in a given year, a scatter plot of the Indirect_Cost_Amount versus the Direct_Cost_Amount reveals points that almost all lie on or below a limiting line. The slope of this line is the indirect cost rate.

Data

The points that lie on the line are those where all direct costs are subject to indirect costs. The points that lie below the line are those where the modified total direct costs (MTDCs) are less than the total direct costs.

Using this approach (with confirmation from internet searches), I compiled the negotiated indirect cost rates for the top 100 institutions in terms of annual NIH funding for fiscal year 2024. I also calculated the indirect cost recovery percentages for these institutions (total indirect costs) / (total direct costs + total indirect costs). The results are shown below and in the file (link):

Estimated Indirect Rates for Fiscal Year 2024 derived from NIH Reporter Data

(Sorted based on decreasing grant funding received)

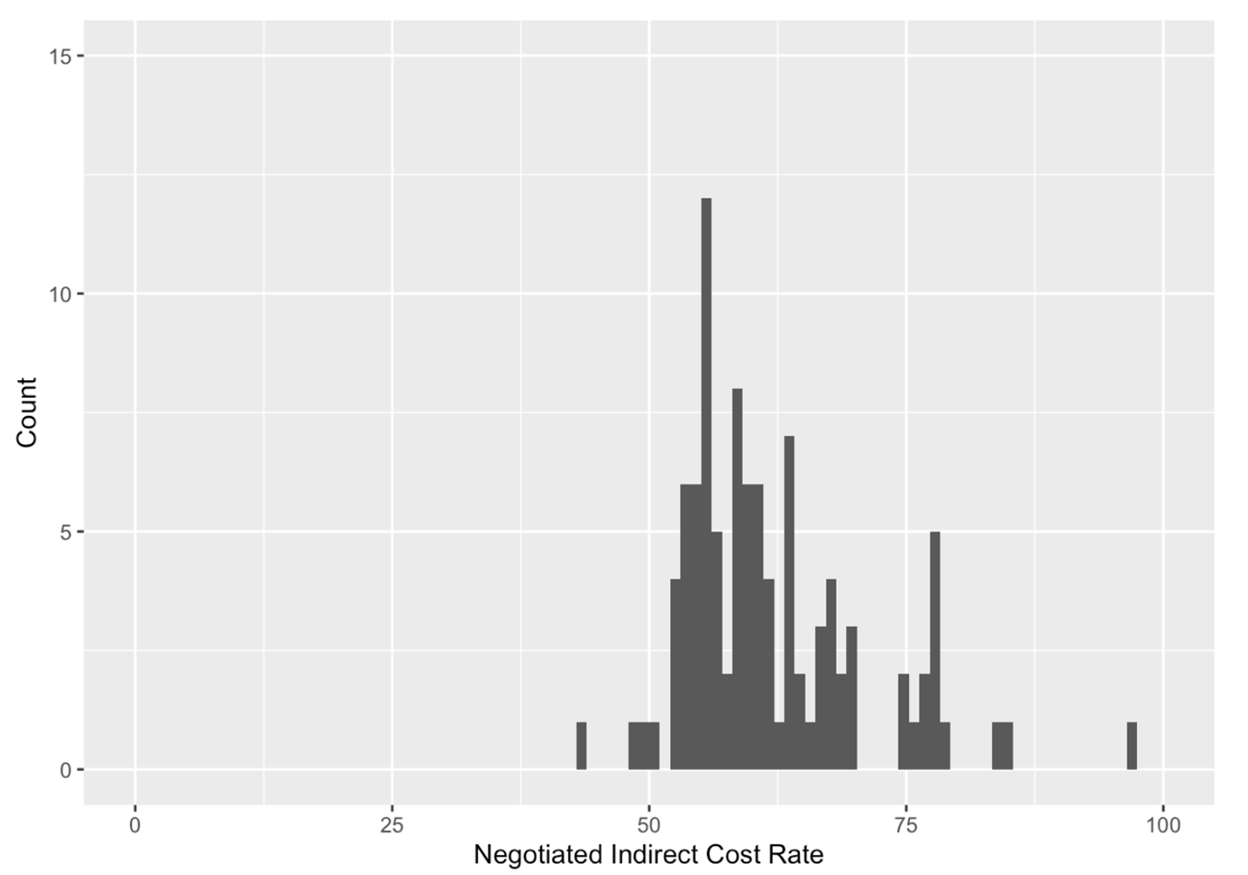

The distribution of these negotiated indirect cost rates is shown below:

This histogram reveals that these rates range from 43.0% to 96.9%.

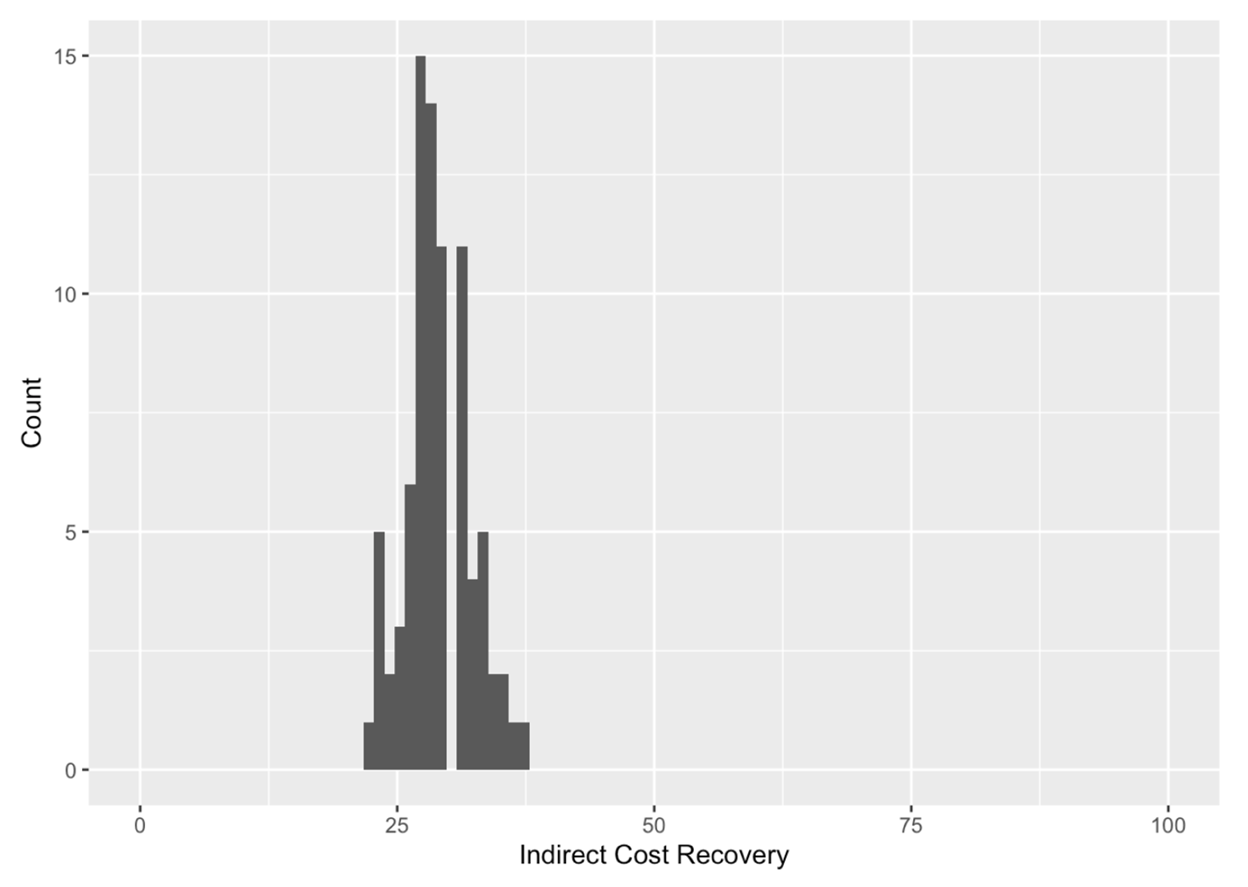

However, examination of actual indirect cost recoveries reveals a somewhat different picture:

The distribution is much tighter, with a range with a range of 21.8% to 37.0%, median of 28.9%, mean of 29.1% and standard deviation of 3.0.

This analysis reveals the basis for the statements in the February 7th notice. Negotiated indirect cost rates do vary substantially from institution to institution, but the actual indirect cost recovery is much lower and much more tightly clustered.

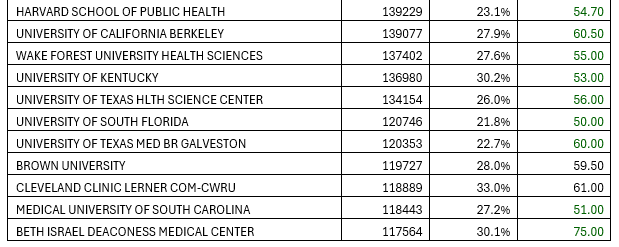

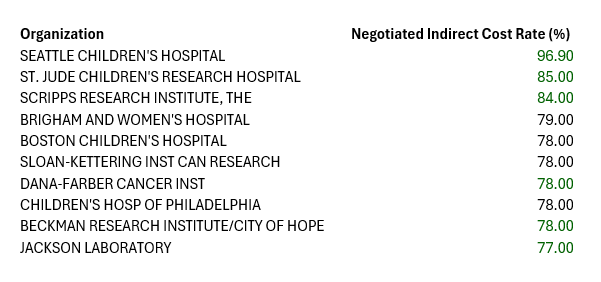

The top 10 institutions with the highest negotiated indirect cost rates are:

These are all free-standing hospitals or independent research institutes, not subject to the 26% cap on administrative cost reimbursement. Despite these high negotiated rates, the actual indirect cost recoveries range from 30.4% to 37.0%, only slightly higher than from institutions with lower negotiated rates.

Alternative Indirect Cost Reimbursement Plans

Because of the controversy around indirect costs, alternative models for accounting and reimbursement are under active development. One of these is the so-called FAIR (Financial Accountability in Research) model. The primary goal of this model is to have indirect cost reimbursement be justified on a grant-by-grant basis rather than at an institutional level, at the expense of substantial additional accounting required by applicants. It is not clear whether this model will decrease, increase, or keep constant actual indirect cost reimbursements.

The NIH Director has also made comments that “market forces” might be used to allow institutions to compete based on lower indirect cost rates (which would then be taken account in making funding decisions); few details have been provided. It is not clear if institutions might choose to appear more competitive by underbidding their actual indirect costs. Since these costs are real, increasing the institutional level of federal funding while losing money on every new grant does not seem to be a robust business model.

In any event, Congress would have to act to approve any model that differs from the current model. It is unclear how these issues will surface during the current appropriation processes.

Policy Recommendation Principles

In considering possible modifications to indirect cost policies, several principles seem important:

First, indirect costs are real research costs. One cannot do research in a sustainable way with laboratory space that is maintained, access to journals, appropriate administrative support for animal and human subject protection, and so on. Those costs could be transferred from indirect to direct costs but with no cost savings for anyone and, likely, increased administrative burden.

Second, increase transparency for all parties would be beneficial for generating support understanding and support. I would favor institutions being required on public websites to post their indirect cost rate information in a manner at least as detailed as that posted by Princeton shown previously. Moreover, a website should be developed with indirect cost rates posted, updated whenever they are renegotiated. This would not require extensive infrastructure to achieve if all institutions were compelled to cooperate. These are, after all, taxpayer funds that are being committed.

With those principles in mind, I am agnostic about the current model versus the FAIR model (which, again, does away with indirect cost rates pe se, but required indirect costs to be estimated for each grant. It may not be possible to sustain the current model due to the damage done through decades of lack of transparency although, in my view, it was a successful early effort aimed at governmental efficiency. The FAIR model has the advantage that the indirect costs for each grant could be examined and audited. However, this would come at the expense of increased administrative burden that could fall on investigators, depending on how the FAIR model is implemented at each institution.

While there are few detailed about the “market forces” plan, if I am correct that the plan would allow institutions to propose indirect cost rates that they would be willing to accept, then I have substantial concerns. First, indirect costs are real research costs that have to come from somewhere and institutions already have some pressure to manage these costs effectively (since indirect cost reimbursements do not fully cover indirect costs). Thus, the need to compete based on lower indirect cost rates could encourage lower levels of building maintenance, decreases in library offerings, cutting administrative activities related to animal care and patient safety, and so on. This would not benefit research in the long run. In addition, it is unclear if this would benefit institutions that currently have lower indirect cost rates as some institutions with substantial other funding to support their research activities might be able to afford relatively low bids.

Let me close with a comment about the rationale for the February 7th NIH notice. This notice stated:

Most private foundations that fund research provide substantially lower indirect costs than the federal government, and universities readily accept grants from these foundations. For example, a recent study found that the most common rate of indirect rate reimbursement by foundations was 0%, meaning many foundations do not fund indirect costs whatsoever. In addition, many of the nation’s largest funders of research—such as the Bill and Melinda Gates Foundation—have a maximum indirect rate of 15%. And in the case of the Gates Foundation, the maximum indirect costs rate is 10% for institutions of higher education.

There are two problems with this argument, one factual and one numerical. As a matter of fact, not all universities and research institutions accept foundation grants that provide low levels of indirect cost reimbursements. A small number of institutions choose to forgo research opportunities for their investigators instead if they do not come with something close to full negotiated indirect cost rates.

The numerical argument relates to scale. Suppose that you are at an institution that is approximately 50th in NIH funding with has $170 million of total cost in federal funding, an indirect cost rate of 56.0%, and an indirect cost recovery of 28.0%. In addition, your institution receives $10 million in direct costs of foundation funding with an indirect cost rate of 15%.

The total amount of indirect costs received would be (0.28 * $170 million) + (0.15 * $10 million) = $47.6 million + $1.5 million = $49.1 million

Declining to accept the $10 million in foundation funding would reduce the total research budget by $11.5 million (out of $181.5 million) and indirect cost recovery from $49.1 million to $47.6 million and would mean the loss of potentially important research projects.

Now supposed that the federal indirect cost rate was unilaterally reduced to 15%. Further assume that this rate applies to all direct cost without modification, the most favorable (for institutions) interpretation of the ambiguous February 7th notice. I will not go through the algebra, but this would mean that the federal indirect costs recovered would be reduced to $18.36 million, a loss of $29.24 million. If, instead, the indirect cost rate applied only to the modified total direct costs, the indirect costs recovered would be reduced further to $12.75 million and a total loss of $34.85 million. These represent very substantial reductions out of a total research budget of $170 to $181.5 million.

This calculation reveals why institutions acted so quickly and aggressively to bring litigation to stop implementation of the 15% indirect cost cap, namely that this would have led to 15-20% reductions in total research budgets with real cost gaps to make up with non-federal funds. As well, they brought litigation quickly because the unilateral change in indirect cost policy without the involvement of Congress was clearly illegal.

Berg's technical corrections to the February 7 notice are valid—the rate/recovery conflation was genuinely sloppy, and the unilateral cap was legally indefensible. But the piece inadvertently commits a category error worth naming: "these costs are real" ≠ "these costs are efficiently produced." Those are separate questions, and the second one never gets asked.

The deeper issue is incentive architecture. No compliance officer's performance metric is "reduced cost per grant dollar"—it's "zero audit findings" and "complete submissions." That's adversarial to efficiency by design. Once a compliance FTE line gets established, it generates its own justification, and nobody in the system is rewarded for repeal, only for reinforcement. Uniform indirect rates then pool labs with radically different actual compliance burdens, obscuring cross-subsidization that benefits the AMC's revenue model while remaining opaque to the investigator paying for it.

This is Yudkowsky's interlocking equilibria problem applied to institutional overhead: regulators add rules in response to visible fraud; AMCs over-respond with compliance layers; compliance offices multiply because the incentive is risk-avoidance not cost minimization; overhead locks in as fixed cost; higher rates are then "negotiated" between two parties who share an interest in opacity. There's no representative of the scientist or taxpayer at that table.

It's also Ezra Klein's Nader Raiders problem. The original regulatory expansions were genuinely reform-motivated. The cumulative sediment forty years later is a compliance regime whose administrative cost may substantially exceed its fraud-prevention value—and whose primary beneficiaries are the compliance infrastructure itself. That's not an argument for DOGE-style blunt-force cuts, which were a fiasco precisely because they ignored these distinctions. It's an argument for what DOGE should have been: menu-priced, line-item overhead transparency that switches the incentive from cost-maximization to cost-minimization. Small businesses and non-profits do this routinely.

The system isn't corrupt. It's misaligned. Those require different fixes.